Reading the at-home biomarker M&A wave

Seven moves in seven months, and what they tell us about layers, lock-in, and the limits of building on Quest.

This is the second piece in the Late Night Convo series. The first one was about us — how we are rebuilding Biostarks as an AI-native at-home biomarker testing company. This one is about the rest of the category, which has been moving fast enough that it's worth writing down what I think is actually happening.

The seven moves

Between September 2025 and April 2026, seven major moves reshaped the at-home biomarker category.

- September 2025 — WHOOP launches Advanced Labs. Clinician-reviewed bloodwork via Quest Diagnostics, 65 biomarkers, integrated with continuous wearable data, 350,000+ waitlist since the May preview. Subsequent extensions — global upload support in November 2025, a Women's Health panel in March 2026 — built on the same architecture without changing the strategic posture.

- October 2025 — Oura launches Health Panels. One day after WHOOP. Different shape of bet: $99 for 50 cardiometabolic biomarkers, Quest for the draw, SteadyMD as the ordering-physician layer, results and AI Advisor interpretation inside the Oura app. Cheaper, narrower, no subscription bundle. Two of the largest wearable companies commit to the blood panel as a core feature in the same week.

- December 2025 — Hims & Hers signs to acquire YourBio Health. TAP device and HALO microneedle technology — bladeless microneedles thinner than an eyelash, capillary sampling in seconds, virtually no pain. Telehealth platform buys the sampling layer outright.

- March 2026 — Herbalife agrees to acquire Bioniq. $55M upfront plus up to $95M contingent on future performance. A legacy nutrition distribution business repositions as a data-driven personalization platform, with Cristiano Ronaldo as the bridge.

- March 2026 — Alan acquires Aro and launches Alan Précision. A European digital insurer turns biomarker testing into an insurance-adjacent product. 80 biomarkers, twice a year, distributed through the health plan.

- April 2026 — Function Health acquires Getlabs. Mobile phlebotomy. Members can now choose a Quest visit or an at-home draw at signup, with AI-assisted routing. Function already running $365/year for 160+ tests with biannual testing built in.

- April 2026 — WHOOP launches Specialized Panels. Five one-time, $299 panels — Heart Health, Performance, Metabolic Health, Women's Health, Men's Health — across 75–89 biomarkers each. FSA/HSA eligible. No subscription required. The first meaningful unbundling of the wearable-plus-labs model into standalone panels that compete directly with Function's domain-specific offerings.

If you lined the architecture diagrams up next to each other, they would be the same shape: sampling → structured biomarkers → AI interpretation → personalized intervention loop. A wearable company, a telehealth platform, a supplement distributor, a health insurer, and a DTC testing brand have all converged on exactly the same product architecture.

What differs is the wedge. But before the wedge, there's a broader direction underneath all seven moves.

The bigger shift: health is moving home

Three of the seven moves above — Hims/YourBio, Function/Getlabs, and arguably the WHOOP+Oura asset-light call to keep Quest as the partner — are in service of the same broader shift. Health, in the consumer wellness segment, is leaving the clinic.

Hims paid for YourBio because the TAP device lets a member draw their own blood at home, painlessly, in seconds. Function paid for Getlabs because mobile phlebotomy means the phlebotomist comes to your kitchen instead of you driving to a Quest patient service centre. Bioniq has shipped DBS-style kits as part of its workflow for years. The entire collection layer of the at-home biomarker stack is being rebuilt around the assumption that you should not have to leave your house.

This isn't unique to biomarker testing. Technogym — the premium gym equipment maker that has historically sold to commercial operators like gyms, hotels, and sports facilities — closed FY 2025 at €1.019 billion in revenue, with the retail channel growing 48.4% in H1 2025 and becoming the fastest-growing part of the business. A B2B-by-DNA company is now seeing its consumer/home segment outpace everything else. The signal is consistent: home is where the category is moving.

Stitch the three together — at-home blood collection, at-home premium fitness equipment, at-home wearable monitoring — and the consumer-side health proposition is no longer "go somewhere to take care of your health." It's "your health context comes to you."

This is what the M&A wave is really aimed at. The brand-layer M&A targets — sampling devices, mobile phlebotomy, on-body sensors — are all collection-side acquisitions. They're how each player commits to the at-home thesis without building the underlying capability themselves. And it's why the friction points start to matter so much: if your value proposition is "we come to you," then every additional layer of dependency that slows you down — every middleware, every lab partner, every regulatory regime per market — becomes a question of whether the at-home promise actually scales.

The product is the same. The wedge is different.

The wedge tells you almost everything about the business model. Four distinct entry points into the same architecture.

Wearable-first. WHOOP and Oura. Both launched blood panels within 24 hours of each other and took different bets on the price/depth curve — WHOOP at $299 per specialty panel plus subscription, Oura at $99 for a single cardiometabolic baseline. Same underlying logic: start with continuous passive data, layer episodic blood on top, make biomarker testing the retention lever for a subscription that was already there. The blood panel is not the product — it's the reason the wearable subscription keeps renewing.

DTC consumer-first. Function Health, Superpower, Hims & Hers on the testing side. Start with the direct consumer relationship, compete on interpretation quality, AI experience, price, and breadth. The blood panel is the product, and everything else — coaching, recommendations, adjunctive tests — is a consequence of owning that relationship.

Nutrition-distribution-first. Herbalife acquiring Bioniq, with Cristiano Ronaldo bridging the two. Use biomarker data to justify personalized supplement formulations, run the economics on supplement margins rather than testing margins. The blood panel is an input that legitimizes a higher-ASP nutrition product downstream.

Payer-first. Alan. The blood panel is a distribution play. The insurer doesn't reimburse the test — as we'll see later, the member still pays — but the insurer owns the channel, the retention logic, and the downstream claims upside. The customer isn't just the insured member; it's the whole incentive system around them.

Four different economic logics, one shared product shape. That alone would be an interesting piece. But the more structurally important observation is not about how different these plays are. It's about how dependent most of them are on infrastructure they don't control.

But look under the hood

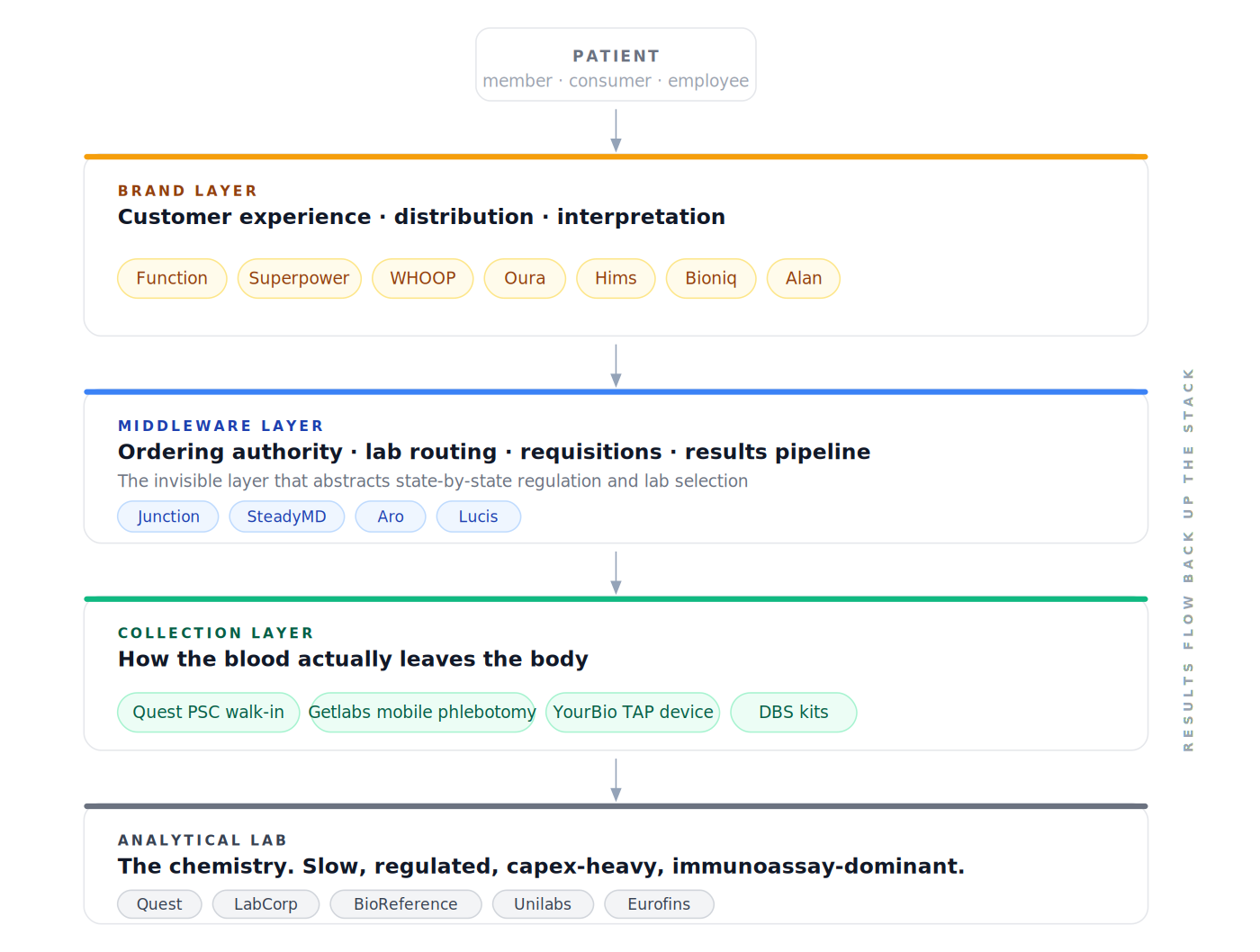

Here is what five of the seven names above actually share: they are brand layers on top of a stack they don't own.

The stack, roughly:

Function and Superpower do not talk directly to Quest or LabCorp. They route through Junction, which provides the licensed-physician network that owns the ordering authority, the API that decides — based on the patient's ZIP code, the state-level compliance constraints, and the account's configured capabilities — whether a given order goes to Quest, LabCorp, or BioReference, the requisition generation, and the results pipeline. Oura's version of this is SteadyMD, which plays a similar ordering-authority and clinical-oversight role for its Health Panels feature. Different names, same layer.

Each layer takes a cut. Each layer inherits the pace of the layer below it.

I want to be careful here, because the easy version of this argument is that layers are bad and the companies building on them are "not really" doing the work. That would be wrong. Layers exist for good reasons.

The brand layer wants to focus on CX and GTM. That is where the real competition happens day to day, and stripping a Function or a Superpower of their UX and onboarding and interpretation layer and saying "but the chemistry is done by Quest" is like saying Stripe is just a wrapper on Visa. It's technically true and it misses why the category exists.

The middleware layer — Junction, in this case — abstracts away the regulatory complexity that would otherwise eat months out of every brand's roadmap: finding licensed physicians, securing ordering authority in fifty different state regimes, generating compliant requisitions, handling critical-value escalation. That is real infrastructure work. It is also work that every brand layer would otherwise have to repeat, badly.

The collection layer is logistics. The analytical layer is chemistry. Specialization is rational. The stack works.

The interesting question is not whether layers are good or bad. It's which layer you choose to compete on, because that choice determines what kind of company you can be.

What's actually being verticalized — and what can't be

Look at the M&A wave with the stack in mind, and the pattern sharpens.

- Function / Getlabs — not a new layer, but an extension of the logistics layer in service of the at-home thesis. Mobile phlebotomy comes to the member instead of the member driving to Quest.

- Herbalife / Bioniq — the personalized outcome. Biomarker data feeds into personalized supplement formulations; the testing is the input, the supplement is the product sold.

- Alan / Aro — not, as a casual read might suggest, an analytical-lab acquisition. What Alan actually bought is access to a network of French labs (Eurofins), with Aro acting as the French-market middleware — essentially Junction for France. That's a market-access move, not a move down the stack.

Nobody bought a major lab incumbent. They are the 800-pound gorillas at the bottom of the stack, and the wave of vertical integration is happening around them, not into them. Two architectural consequences follow — and the press releases don't mention either.

The geography ceiling

Transactions in this space are built to secure access to the lab network and to add new collection modalities. But the incumbent lab network forces the brand layer to integrate per region. Global scale at the brand layer doesn't buy global scale at the lab layer.

- Alan now serves five markets across Europe — France, Belgium, Spain, Canada, and more — but only built lab access in France via Aro, and even there the coverage is partial. The other Alan markets don't yet have Précision. Cross-border rollout is a per-market lab partnership problem.

- Oura ships 5.5M rings globally, but Health Panels is US-only in the US and requires parallel regional partnerships everywhere else — Unilabs in the UAE, other labs in other markets. Every market reopens the interpretation layer. The pipeline that works cleanly on a Quest PDF in Texas doesn't translate one-to-one to a Unilabs PDF in Dubai. A friend recently showed me the Oura output from a Unilabs UAE draw: the interpretation depth was visibly thinner than the US-native experience, not because the pipeline is poor, but because it was tuned for one lab's outputs and hasn't fully relearned the other.

The innovation ceiling

Even inside a single market, brand-layer plays are constrained by what their incumbent lab can physically run. Quest, LabCorp, Unilabs, and their peers are immunoassay-heavy — their analytical infrastructure is optimized for a specific set of chemistries deployed at scale across hundreds of physical collection centres. They are unlikely, in the near term, to retrofit mass spectrometry or other advanced assay technologies into that footprint. The ROI for them is in throughput, not in panel breadth.

Which means the brand layer can ship a better interpretation screen this quarter, but it can't meaningfully expand panel coverage beyond what the incumbent lab's existing hardware already runs. The innovation ceiling of the brand layer is the innovation floor of the lab layer. If the future of precision health involves assays that immunoassay labs don't currently run, the brand layer will not be the one to introduce them — it will have to wait for the lab to get there.

The structural cost, and a different bet

Put the two ceilings together and the structural cost of starting at the brand layer and building downward through incumbent lab infrastructure is visible. You inherit US speed on the way up — Function went from zero to millions of members in a few years, which would not have been possible without Quest and Junction doing the work below them — and you inherit US-only reach on the way out, with a slow-moving assay roadmap even at home.

In hindsight, this is a big part of why we are starting Biostarks with a B2B open-platform model rather than a US-style DTC rollout. We are a Geneva-based company. We do not have a domestic stack to build on. The moment you build for international operation, you cannot afford to be the fourth layer on top of Function on top of Junction on top of Quest — because that whole tower does not exist outside the US, and it would have to be reassembled per market with different incumbents at each layer.

So you go upstream instead of downstream: own the substrate (sampling, analysis, interpretation), build it once, and offer it as an open platform that brand-layer partners — wellness apps, nutrition platforms, insurers, employers, fitness operators — can plug into without rebuilding the lower stack themselves. The brand layer wins on customer experience and distribution. The platform layer wins by being the rails that everyone else builds on.

Starting upstream is harder, slower, and more capex-heavy than starting at the brand layer. The US brand-layer plays are growing faster than we are on every surface metric. They should be — they skipped the hardest part of the problem. But if you ask which of these models ports to five continents, the answer is not Function and not WHOOP Advanced Labs. It's the model that does not depend on US-only plumbing — or on incumbent-lab roadmaps.

The most underestimated move on the list

Of the seven moves, the one I think most of the category is underestimating is Alan Précision. WHOOP just inadvertently published the actuarial argument for it.

Among an already active WHOOP population, 22% show signs of metabolic dysfunction and nearly 30% have underlying cardiometabolic risk factors, often without prior awareness.

That number is from the WHOOP Specialized Panels launch. Keep in mind it is measured on a selected population — people who already bought a premium wearable, care about their health enough to wear it daily, and are active enough to generate useful data. If 22%–30% of that population has unrecognized cardiometabolic risk, the prevalence across a general insured population is not lower.

The first thing to get right about Alan Précision is the pricing model, because the easy assumption — and the one I made when I first saw the announcement — is that the insurer underwrites the test. They don't. The member pays out of pocket. Alan has slashed the price to €249 per panel, twice a year (so roughly €500 per year if both are taken), and the test is not reimbursed. That's the structural innovation: not "free preventive testing as part of your insurance," but "preventive testing made cheap because your insurer is the distribution channel."

Compare the price points:

- Function Health: ~$365/year, biannual, 160+ markers via Quest

- WHOOP Specialized Panels: $299 per one-time panel, 75–89 markers via Quest

- Aro retail (pre-acquisition, comparable Swiss/French market): in the €400–500 range per panel

- Alan Précision: €249 per panel, 80+ markers, integrated into a 1.1M-member insurance distribution

Alan can offer this price because the customer acquisition cost is amortized across the insurance product, and because the insurer has aligned incentives downstream. Healthier members make fewer claims. Engaged members renew their insurance contract. Even at break-even on the test itself, the integration with the insurance experience is its own moat.

That is structurally different from everyone else on the list.

- The DTC plays need the consumer to keep paying €365/year as a wellness subscription.

- The wearable plays need the wearable subscription to keep renewing on its own merits.

- The nutrition plays need supplements to keep shipping at premium ASPs.

- The payer play has the testing as a near-cost loss leader, with the upside captured upstream (insurance retention, brand trust) and downstream (claims reduction).

What would have to be true for the Alan model to actually work?

- Member adoption at €249 has to be significantly better than at retail prices. This is testable in quarters, not years. Alan is presumably already running this experiment. The bet is that pulling price from €400+ down to €249 unlocks a behaviourally different segment — not the wellness-curious early adopter, but the average insured member who wouldn't have considered preventive testing at €400. If adoption uplift is meaningful and engaged members renew their insurance contract at a higher rate, the model is validated on the retention side alone.

- The biomarker → behaviour change → outcome chain has to be tight enough to show up in claims data. This is not yet proven at scale for asymptomatic populations. Individual case studies exist; population-level claims impact does not yet.

The first is tractable in 12–18 months of internal data. The second is a multi-year question and is the slowest-moving variable.

But the first condition alone is enough. If adoption uplift shows up in the first year, Alan doesn't need to wait for claims data to move the category — every other digital insurer in Europe is already watching. If the model holds, the European insurer pack will copy it within twelve months and US Medicare Advantage plans will follow within twenty-four. The DTC plays compete with retail wellness budgets. The payer play resets what "retail" looks like. That's why Alan Précision is the move I think the category is most underestimating: not because it's the biggest, but because it's the one that, if it works, doesn't just succeed on its own — it changes the unit economics of everything else on the list.

What I'm watching for

A few things I'm actively tracking as an operator in this space.

Whether the brand-layer plays keep consolidating their stack. Function buying Getlabs is a signal. Hims buying YourBio is a signal. Both moves reached for the collection layer, which is the easiest part of the stack to acquire outright. The more revealing move would be a brand-layer play acquiring an analytical lab — or funding one to scale. I don't think any of the named players will move on Quest or LabCorp directly; those are not for sale. But the scale-up tier below them — specialty labs, mass-spec shops, regional reference labs — is very much in play.

Whether the middleware layer monetizes its leverage. Right now Junction and SteadyMD are invisible to end customers and known only to the brands building on them. As the brand layer commoditizes on CX, the leverage shifts to the layer below. The open question is whether that middleware monetizes aggressively, stays an enabler, or gets disintermediated by a brand-layer player deciding to build its own ordering-authority and routing infrastructure.

Whether an equivalent substrate emerges outside the US. The geography ceiling above is a market structure that isn't going to fix itself. If a regional player builds a credible analytical-and-ordering substrate for European brands, the WHOOP and Function look-alikes in Europe will plug into it as fast as their US counterparts plugged into Junction. If nobody builds it, the European market stays structurally different — more vertically integrated by force, smaller national players, more partnerships per company.

The strategic topology of the next five years in this category gets set at the layer below the brand. Which lab infrastructure ports internationally. Whether the middleware commoditizes or aggregates. Whether a payer model proves out and resets the category's pricing gravity. Whether an analytical-layer substrate emerges outside the US. Most of the industry conversation right now happens at the brand layer, because that is where the marketing, the consumer stories, and the venture valuations sit. But the layer where the moves matter most is the one underneath.

If you are building in this category and you disagree, I'd like to hear it. Particularly if you are building at a layer I did not get right.

More updates as the landscape moves.

— Romain Dorange, CEO & Co-Founder, Biostarks

This is the second in the Late Night Convo series on building an AI-native at-home biomarker testing company. The first is here.